The Internal Revenue Service (IRS) has recently released new data on individual income taxes for taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. year 2016, showing the number of taxpayers, adjusted gross incomeFor individuals, gross income is the total of all income received from any source before taxes or deductions. It includes wages, salaries, tips, interest, dividends, capital gains, rental income, alimony, pensions, and other forms of income. For businesses, gross income (or gross profit) is the sum of total receipts or sales minus the cost of goods sold (COGS)—the direct costs of producing goods, and income tax shares by income percentiles.[1]

The data demonstrates that the U.S. individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source continues to be very progressive, borne primarily by the highest income earners.[2]

- In 2016, 140.9 million taxpayers reported earning $10.2 trillion in adjusted gross income and paid $1.4 trillion in individual income taxes.

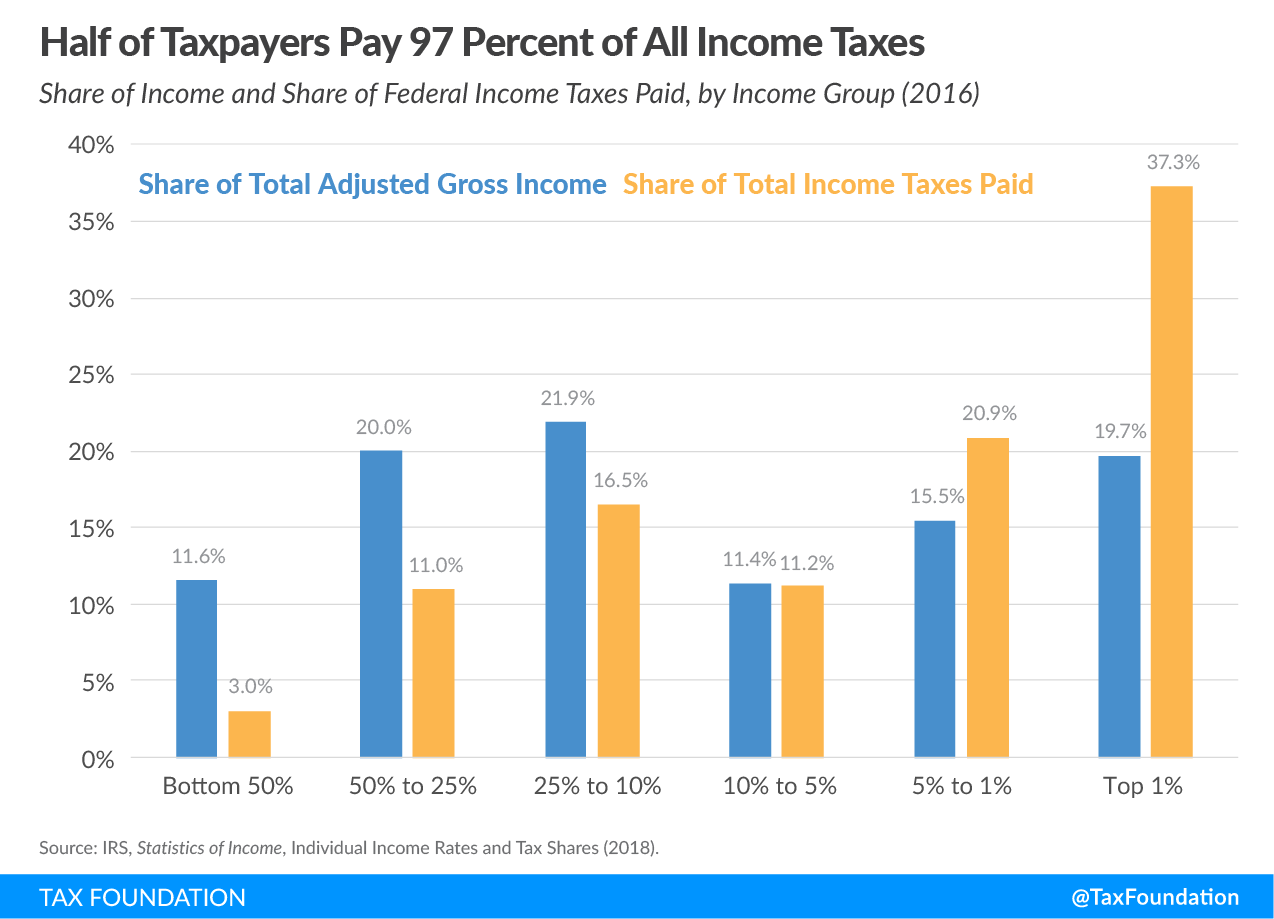

- The share of reported income earned by the top 1 percent of taxpayers fell slightly to 19.7 percent in 2016. Their share of federal individual income taxes fell slightly, to 37.3 percent.

- In 2016, the top 50 percent of all taxpayers paid 97 percent of all individual income taxes, while the bottom 50 percent paid the remaining 3 percent.

- The top 1 percent paid a greater share of individual income taxes (37.3 percent) than the bottom 90 percent combined (30.5 percent).

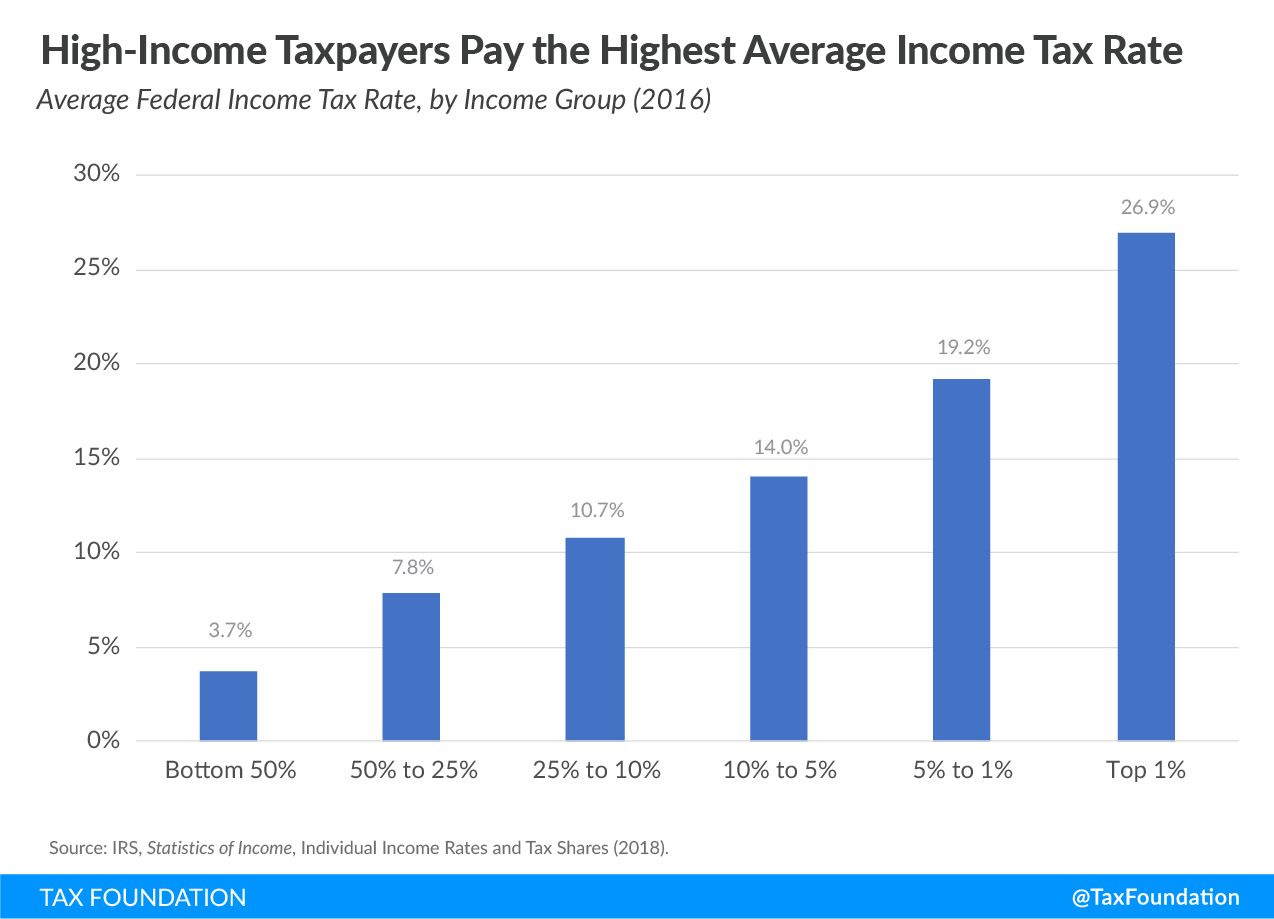

- The top 1 percent of taxpayers paid a 26.9 percent individual income tax rate, which is more than seven times higher than taxpayers in the bottom 50 percent (3.7 percent).

Reported Income Increased and Taxes Paid Decreased in 2016

Taxpayers reported $10.2 trillion in adjusted gross income (AGI) on 140.9 million tax returns in 2016. Total AGI grew $14 billion from 2015 levels, less than the $434 billion increase from 2014 to 2015. There were 316,000 fewer tax returns filed in 2016 than in 2015, meaning that average AGI rose by $260 per return, or 0.4 percent.

Taxes paid fell slightly to $1.4 trillion for all taxpayers in 2016, a 0.8 percent decrease from the previous year. The average individual income tax rate for all taxpayers fell slightly, from 14.3 percent to 14.2 percent, and the average tax rate fell for all groups.

The share of income earned by the top 1 percent fell slightly from 20.7 percent of AGI in 2015 to 19.7 percent in 2016, and the share of the income tax burden for the top 1 percent fell slightly as well, from 39 percent in 2015 to 37.3 percent in 2016.

| Note: Table does not include dependent filers. “Income split point” is the minimum AGI for tax returns to fall into each percentile. Source: IRS, Statistics of Income, Individual Income Rates and Tax Shares (2018). | ||||||||

| Top 1% | Top 5% | Top 10% | Top 25% | Top 50% | Bottom 50% | All Taxpayers | ||

|---|---|---|---|---|---|---|---|---|

| Number of Returns | 1,408,888 | 7,044,439 | 14,088,879 | 35,222,196 | 70,444,393 | 70,444,393 | 140,888,785 | |

| Adjusted Gross Income ($ millions) | $2,003,066 | $3,574,828 | $4,729,405 | $6,950,051 | $8,979,705 | $1,176,907 | $10,156,612 | |

| Share of Total Adjusted Gross Income | 19.72% | 35.20% | 46.56% | 68.43% | 88.41% | 11.59% | 100.00% | |

| Income Taxes Paid ($ millions) | $538,257 | $839,898 | $1,002,072 | $1,240,010 | $1,398,523 | $43,863 | $1,442,385 | |

| Share of Total Income Taxes Paid | 37.32% | 58.23% | 69.47% | 85.97% | 96.96% | 3.04% | 100.00% | |

| Income Split Point | $480,804 | $197,651 | $139,713 | $80,921 | $40,078 | |||

| Average Tax Rate | 26.87% | 23.49% | 21.19% | 17.84% | 15.57% | 3.73% | 14.20% | |

High-Income Taxpayers Paid Majority of Federal Income Taxes

In 2016, the bottom 50 percent of taxpayers (those with AGI below $40,078) earned 11.6 percent of total AGI. This group of taxpayers paid $43.9 billion in taxes, or roughly 3 percent of all income taxes in 2016.

In contrast, the top 1 percent of all taxpayers (taxpayers with AGI of $480,804 and above), earned 19.7 percent of all AGI in 2016, and paid 37.3 percent of all federal income taxes.

In 2016, the top 1 percent of taxpayers accounted for more income taxes paid than the bottom 90 percent combined. The top 1 percent of taxpayers paid roughly $538 billion, or 37.3 percent of all income taxes, while the bottom 90 percent paid about $440 billion, or 30.5 percent of all income taxes.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeHigh-Income Taxpayers Paid the Highest Average Income Tax Rates

The 2016 IRS data shows that taxpayers with higher incomes pay much higher average income tax rates than lower-income taxpayers.[3]

The bottom 50 percent of taxpayers (taxpayers with AGIs below $40,078) faced an average income tax rate of 3.7 percent. As household income increases, the IRS data shows that average income tax rates rise. For example, taxpayers with AGIs between the 10th and 5th percentiles ($139,713 and $197,651) paid an average effective rate of 14 percent—3.8 times the rate paid by those in the bottom 50 percent.

The top 1 percent of taxpayers (AGI of $480,804 and above) paid the highest effective income tax rate, roughly 26.9 percent, more than seven times the rate faced by the bottom 50 percent of taxpayers.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeTaxpayers at the very top of the income distribution, the top 0.1 percent (with AGIs over $2.1 million), paid an even higher average income tax rate of 27.1 percent.

Appendix

- For data prior to 2001, all tax returns that have a positive AGI are included, even those that do not have a positive income tax liability. For data from 2001 forward, returns with negative AGI are also included, but dependent returns are excluded.

- Income tax after credits (the measure of “income taxes paid” above) does not account for the refundable portion of the earned income tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly.. If it were included, the tax share of the top income groups would be higher. The refundable portion is classified as a spending program by the Office of Management and Budget and therefore is not included by the IRS in these figures.

- The only tax analyzed here is the federal individual income tax, which is responsible for more than 25 percent of the nation’s taxes paid (at all levels of government). Federal income taxes are much more progressive than federal payroll taxes, which are responsible for about 20 percent of all taxes paid (at all levels of government), and are more progressive than most state and local taxes.

- AGI is a fairly narrow income concept and does not include income items like government transfers (except for the portion of Social Security benefits that is taxed), the value of employer-provided health insurance, underreported or unreported income (most notably that of sole proprietors), income derived from municipal bond interest, net imputed rental income, and others.

- The unit of analysis here is that of the tax return. In the figures prior to 2001, some dependent returns are included. Under other units of analysis (like the U.S. Treasury Department’s Family Economic Unit), these returns would likely be paired with parents’ returns.

- These figures represent the legal incidence of the income tax. Most distributional tables (such as those from the Congressional Budget Office, the Tax Policy Center, Citizens for Tax Justice, the Treasury Department, and the Joint Committee on Taxation) assume that the entire economic incidence of personal income taxes falls on the income earner.

| Source: IRS, Statistics of Income, Individual Income Rates and Tax Shares (2018). | |||||||||||

| Year | Total | Top 0.1% | Top 1% | Top 5% | Between 5% and 10% | Top 10% | Between 10% and 25% | Top 25% | Between 25% and 50% | Top 50% | Bottom 50% |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1981 | 94,587 | 946 | 4,729 | 4,729 | 9,459 | 14,188 | 23,647 | 23,647 | 47,293 | 47,293 | |

| 1982 | 94,426 | 944 | 4,721 | 4,721 | 9,443 | 14,164 | 23,607 | 23,607 | 47,213 | 47,213 | |

| 1983 | 95,331 | 953 | 4,767 | 4,767 | 9,533 | 14,300 | 23,833 | 23,833 | 47,665 | 47,665 | |

| 1984 | 98,436 | 984 | 4,922 | 4,922 | 9,844 | 14,765 | 24,609 | 24,609 | 49,218 | 49,219 | |

| 1985 | 100,625 | 1,006 | 5,031 | 5,031 | 10,063 | 15,094 | 25,156 | 25,156 | 50,313 | 50,313 | |

| 1986 | 102,088 | 1,021 | 5,104 | 5,104 | 10,209 | 15,313 | 25,522 | 25,522 | 51,044 | 51,044 | |

| The Tax Reform Act of 1986 changed the definition of AGI, so data above and below this line is not strictly comparable. | |||||||||||

| 1987 | 106,155 | 1,062 | 5,308 | 5,308 | 10,615 | 15,923 | 26,539 | 26,539 | 53,077 | 53,077 | |

| 1988 | 108,873 | 1,089 | 5,444 | 5,444 | 10,887 | 16,331 | 27,218 | 27,218 | 54,436 | 54,436 | |

| 1989 | 111,313 | 1,113 | 5,566 | 5,566 | 11,131 | 16,697 | 27,828 | 27,828 | 55,656 | 55,656 | |

| 1990 | 112,812 | 1,128 | 5,641 | 5,641 | 11,281 | 16,922 | 28,203 | 28,203 | 56,406 | 56,406 | |

| 1991 | 113,804 | 1,138 | 5,690 | 5,690 | 11,380 | 17,071 | 28,451 | 28,451 | 56,902 | 56,902 | |

| 1992 | 112,653 | 1,127 | 5,633 | 5,633 | 11,265 | 16,898 | 28,163 | 28,163 | 56,326 | 56,326 | |

| 1993 | 113,681 | 1,137 | 5,684 | 5,684 | 11,368 | 17,052 | 28,420 | 28,420 | 56,841 | 56,841 | |

| 1994 | 114,990 | 1,150 | 5,749 | 5,749 | 11,499 | 17,248 | 28,747 | 28,747 | 57,495 | 57,495 | |

| 1995 | 117,274 | 1,173 | 5,864 | 5,864 | 11,727 | 17,591 | 29,319 | 29,319 | 58,637 | 58,637 | |

| 1996 | 119,442 | 1,194 | 5,972 | 5,972 | 11,944 | 17,916 | 29,860 | 29,860 | 59,721 | 59,721 | |

| 1997 | 121,503 | 1,215 | 6,075 | 6,075 | 12,150 | 18,225 | 30,376 | 30,376 | 60,752 | 60,752 | |

| 1998 | 123,776 | 1,238 | 6,189 | 6,189 | 12,378 | 18,566 | 30,944 | 30,944 | 61,888 | 61,888 | |

| 1999 | 126,009 | 1,260 | 6,300 | 6,300 | 12,601 | 18,901 | 31,502 | 31,502 | 63,004 | 63,004 | |

| 2000 | 128,227 | 1,282 | 6,411 | 6,411 | 12,823 | 19,234 | 32,057 | 32,057 | 64,114 | 64,114 | |

| The IRS changed methodology, so data above and below this line is not strictly comparable. | |||||||||||

| 2001 | 119,371 | 119 | 1,194 | 5,969 | 5,969 | 11,937 | 17,906 | 29,843 | 29,843 | 59,685 | 59,685 |

| 2002 | 119,851 | 120 | 1,199 | 5,993 | 5,993 | 11,985 | 17,978 | 29,963 | 29,963 | 59,925 | 59,925 |

| 2003 | 120,759 | 121 | 1,208 | 6,038 | 6,038 | 12,076 | 18,114 | 30,190 | 30,190 | 60,379 | 60,379 |

| 2004 | 122,510 | 123 | 1,225 | 6,125 | 6,125 | 12,251 | 18,376 | 30,627 | 30,627 | 61,255 | 61,255 |

| 2005 | 124,673 | 125 | 1,247 | 6,234 | 6,234 | 12,467 | 18,701 | 31,168 | 31,168 | 62,337 | 62,337 |

| 2006 | 128,441 | 128 | 1,284 | 6,422 | 6,422 | 12,844 | 19,266 | 32,110 | 32,110 | 64,221 | 64,221 |

| 2007 | 132,655 | 133 | 1,327 | 6,633 | 6,633 | 13,265 | 19,898 | 33,164 | 33,164 | 66,327 | 66,327 |

| 2008 | 132,892 | 133 | 1,329 | 6,645 | 6,645 | 13,289 | 19,934 | 33,223 | 33,223 | 66,446 | 66,446 |

| 2009 | 132,620 | 133 | 1,326 | 6,631 | 6,631 | 13,262 | 19,893 | 33,155 | 33,155 | 66,310 | 66,310 |

| 2010 | 135,033 | 135 | 1,350 | 6,752 | 6,752 | 13,503 | 20,255 | 33,758 | 33,758 | 67,517 | 67,517 |

| 2011 | 136,586 | 137 | 1,366 | 6,829 | 6,829 | 13,659 | 20,488 | 34,146 | 34,146 | 68,293 | 68,293 |

| 2012 | 136,080 | 136 | 1,361 | 6,804 | 6,804 | 13,608 | 20,412 | 34,020 | 34,020 | 68,040 | 68,040 |

| 2013 | 138,313 | 138 | 1,383 | 6,916 | 6,916 | 13,831 | 20,747 | 34,578 | 34,578 | 69,157 | 69,157 |

| 2014 | 139,562 | 140 | 1,396 | 6,978 | 6,978 | 13,956 | 20,934 | 34,891 | 34,891 | 69,781 | 69,781 |

| 2015 | 141,205 | 141 | 1,412 | 7,060 | 7,060 | 14,120 | 21,181 | 35,301 | 35,301 | 70,602 | 70,602 |

| 2016 | 140,889 | 141 | 1,409 | 7,044 | 7,044 | 14,089 | 21,133 | 35,222 | 35,222 | 70,444 | 70,444 |

| Source: IRS, Statistics of Income, Individual Income Rates and Tax Shares (2018). | |||||||||||

| Year | Total | Top 0.1% | Top 1% | Top 5% | Between 5% & 10% | Top 10% | Between 10% & 25% | Top 25% | Between 25% & 50% | Top 50% | Bottom 50% |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1980 | $1,627 | $138 | $342 | $181 | $523 | $400 | $922 | $417 | $1,339 | $288 | |

| 1981 | $1,791 | $149 | $372 | $201 | $573 | $442 | $1,015 | $458 | $1,473 | $318 | |

| 1982 | $1,876 | $167 | $398 | $207 | $605 | $460 | $1,065 | $478 | $1,544 | $332 | |

| 1983 | $1,970 | $183 | $428 | $217 | $646 | $481 | $1,127 | $498 | $1,625 | $344 | |

| 1984 | $2,173 | $210 | $482 | $240 | $723 | $528 | $1,251 | $543 | $1,794 | $379 | |

| 1985 | $2,344 | $235 | $531 | $260 | $791 | $567 | $1,359 | $580 | $1,939 | $405 | |

| 1986 | $2,524 | $285 | $608 | $278 | $887 | $604 | $1,490 | $613 | $2,104 | $421 | |

| The Tax Reform Act of 1986 changed the definition of AGI, so data above and below this line is not strictly comparable. | |||||||||||

| 1987 | $2,814 | $347 | $722 | $316 | $1,038 | $671 | $1,709 | $664 | $2,374 | $440 | |

| 1988 | $3,124 | $474 | $891 | $342 | $1,233 | $718 | $1,951 | $707 | $2,658 | $466 | |

| 1989 | $3,299 | $468 | $918 | $368 | $1,287 | $768 | $2,054 | $751 | $2,805 | $494 | |

| 1990 | $3,451 | $483 | $953 | $385 | $1,338 | $806 | $2,144 | $788 | $2,933 | $519 | |

| 1991 | $3,516 | $457 | $943 | $400 | $1,343 | $832 | $2,175 | $809 | $2,984 | $532 | |

| 1992 | $3,681 | $524 | $1,031 | $413 | $1,444 | $856 | $2,299 | $832 | $3,131 | $549 | |

| 1993 | $3,776 | $521 | $1,048 | $426 | $1,474 | $883 | $2,358 | $854 | $3,212 | $563 | |

| 1994 | $3,961 | $547 | $1,103 | $449 | $1,552 | $929 | $2,481 | $890 | $3,371 | $590 | |

| 1995 | $4,245 | $620 | $1,223 | $482 | $1,705 | $985 | $2,690 | $938 | $3,628 | $617 | |

| 1996 | $4,591 | $737 | $1,394 | $515 | $1,909 | $1,043 | $2,953 | $992 | $3,944 | $646 | |

| 1997 | $5,023 | $873 | $1,597 | $554 | $2,151 | $1,116 | $3,268 | $1,060 | $4,328 | $695 | |

| 1998 | $5,469 | $1,010 | $1,797 | $597 | $2,394 | $1,196 | $3,590 | $1,132 | $4,721 | $748 | |

| 1999 | $5,909 | $1,153 | $2,012 | $641 | $2,653 | $1,274 | $3,927 | $1,199 | $5,126 | $783 | |

| 2000 | $6,424 | $1,337 | $2,267 | $688 | $2,955 | $1,358 | $4,314 | $1,276 | $5,590 | $834 | |

| The IRS changed methodology, so data above and below this line is not strictly comparable. | |||||||||||

| 2001 | $6,116 | $492 | $1,065 | $1,934 | $666 | $2,600 | $1,334 | $3,933 | $1,302 | $5,235 | $881 |

| 2002 | $5,982 | $421 | $960 | $1,812 | $660 | $2,472 | $1,339 | $3,812 | $1,303 | $5,115 | $867 |

| 2003 | $6,157 | $466 | $1,030 | $1,908 | $679 | $2,587 | $1,375 | $3,962 | $1,325 | $5,287 | $870 |

| 2004 | $6,735 | $615 | $1,279 | $2,243 | $725 | $2,968 | $1,455 | $4,423 | $1,403 | $5,826 | $908 |

| 2005 | $7,366 | $784 | $1,561 | $2,623 | $778 | $3,401 | $1,540 | $4,940 | $1,473 | $6,413 | $953 |

| 2006 | $7,970 | $895 | $1,761 | $2,918 | $841 | $3,760 | $1,652 | $5,412 | $1,568 | $6,980 | $990 |

| 2007 | $8,622 | $1,030 | $1,971 | $3,223 | $905 | $4,128 | $1,770 | $5,898 | $1,673 | $7,571 | $1,051 |

| 2008 | $8,206 | $826 | $1,657 | $2,868 | $905 | $3,773 | $1,782 | $5,555 | $1,673 | $7,228 | $978 |

| 2009 | $7,579 | $602 | $1,305 | $2,439 | $878 | $3,317 | $1,740 | $5,058 | $1,620 | $6,678 | $900 |

| 2010 | $8,040 | $743 | $1,517 | $2,716 | $915 | $3,631 | $1,800 | $5,431 | $1,665 | $7,096 | $944 |

| 2011 | $8,317 | $737 | $1,556 | $2,819 | $956 | $3,775 | $1,866 | $5,641 | $1,716 | $7,357 | $961 |

| 2012 | $9,042 | $1,017 | $1,977 | $3,331 | $997 | $4,328 | $1,934 | $6,262 | $1,776 | $8,038 | $1,004 |

| 2013 | $9,034 | $816 | $1,720 | $3,109 | $1,034 | $4,143 | $2,008 | $6,152 | $1,844 | $7,996 | $1,038 |

| 2014 | $9,709 | $986 | $1,998 | $3,491 | $1,093 | $4,583 | $2,107 | $6,690 | $1,924 | $8,615 | $1,094 |

| 2015 | $10,143 | $1,033 | $2,095 | $3,659 | $1,145 | $4,803 | $2,194 | $6,998 | $2,000 | $8,998 | $1,145 |

| 2016 | $10,157 | $966 | $2,003 | $3,575 | $1,155 | $4,729 | $2,221 | $6,950 | $2,030 | $8,980 | $1,177 |

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe| Source: IRS, Statistics of Income, Individual Income Rates and Tax Shares (2018). | |||||||||||

| Year | Total | Top 0.1% | Top 1% | Top 5% | Between 5% & 10% | Top 10% | Between 10% & 25% | Top 25% | Between 25% & 50% | Top 50% | Bottom 50% |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1980 | $249 | $47 | $92 | $31 | $123 | $59 | $182 | $50 | $232 | $18 | |

| 1981 | $282 | $50 | $99 | $36 | $135 | $69 | $204 | $57 | $261 | $21 | |

| 1982 | $276 | $53 | $100 | $34 | $134 | $66 | $200 | $56 | $256 | $20 | |

| 1983 | $272 | $55 | $101 | $34 | $135 | $64 | $199 | $54 | $252 | $19 | |

| 1984 | $297 | $63 | $113 | $37 | $150 | $68 | $219 | $57 | $276 | $22 | |

| 1985 | $322 | $70 | $125 | $41 | $166 | $73 | $238 | $60 | $299 | $23 | |

| 1986 | $367 | $94 | $156 | $44 | $201 | $78 | $279 | $64 | $343 | $24 | |

| The Tax Reform Act of 1986 changed the definition of AGI, so data above and below this line is not strictly comparable. | |||||||||||

| 1987 | $369 | $92 | $160 | $46 | $205 | $79 | $284 | $63 | $347 | $22 | |

| 1988 | $413 | $114 | $188 | $48 | $236 | $85 | $321 | $68 | $389 | $24 | |

| 1989 | $433 | $109 | $190 | $51 | $241 | $93 | $334 | $73 | $408 | $25 | |

| 1990 | $447 | $112 | $195 | $52 | $248 | $97 | $344 | $77 | $421 | $26 | |

| 1991 | $448 | $111 | $194 | $56 | $250 | $96 | $347 | $77 | $424 | $25 | |

| 1992 | $476 | $131 | $218 | $58 | $276 | $97 | $374 | $78 | $452 | $24 | |

| 1993 | $503 | $146 | $238 | $60 | $298 | $101 | $399 | $80 | $479 | $24 | |

| 1994 | $535 | $154 | $254 | $64 | $318 | $108 | $425 | $84 | $509 | $25 | |

| 1995 | $588 | $178 | $288 | $70 | $357 | $115 | $473 | $88 | $561 | $27 | |

| 1996 | $658 | $213 | $335 | $76 | $411 | $124 | $535 | $95 | $630 | $28 | |

| 1997 | $727 | $241 | $377 | $82 | $460 | $134 | $594 | $102 | $696 | $31 | |

| 1998 | $788 | $274 | $425 | $88 | $513 | $139 | $652 | $103 | $755 | $33 | |

| 1999 | $877 | $317 | $486 | $97 | $583 | $150 | $733 | $109 | $842 | $35 | |

| 2000 | $981 | $367 | $554 | $106 | $660 | $164 | $824 | $118 | $942 | $38 | |

| The IRS changed methodology, so data above and below this line is not strictly comparable. | |||||||||||

| 2001 | $885 | $139 | $294 | $462 | $101 | $564 | $158 | $722 | $120 | $842 | $43 |

| 2002 | $794 | $120 | $263 | $420 | $93 | $513 | $143 | $657 | $104 | $761 | $33 |

| 2003 | $746 | $115 | $251 | $399 | $85 | $484 | $133 | $617 | $98 | $715 | $30 |

| 2004 | $829 | $142 | $301 | $467 | $91 | $558 | $137 | $695 | $102 | $797 | $32 |

| 2005 | $932 | $176 | $361 | $549 | $98 | $647 | $145 | $793 | $106 | $898 | $33 |

| 2006 | $1,020 | $196 | $402 | $607 | $108 | $715 | $157 | $872 | $113 | $986 | $35 |

| 2007 | $1,112 | $221 | $443 | $666 | $117 | $783 | $170 | $953 | $122 | $1,075 | $37 |

| 2008 | $1,029 | $187 | $386 | $597 | $115 | $712 | $168 | $880 | $117 | $997 | $32 |

| 2009 | $863 | $146 | $314 | $502 | $101 | $604 | $146 | $749 | $93 | $842 | $21 |

| 2010 | $949 | $170 | $355 | $561 | $110 | $670 | $156 | $827 | $100 | $927 | $22 |

| 2011 | $1,043 | $168 | $366 | $589 | $123 | $712 | $181 | $893 | $120 | $1,012 | $30 |

| 2012 | $1,185 | $220 | $451 | $699 | $133 | $831 | $193 | $1,024 | $128 | $1,152 | $33 |

| 2013 | $1,232 | $228 | $466 | $721 | $139 | $860 | $203 | $1,063 | $135 | $1,198 | $34 |

| 2014 | $1,374 | $273 | $543 | $824 | $150 | $974 | $219 | $1,193 | $144 | $1,337 | $38 |

| 2015 | $1,454 | $284 | $568 | $866 | $160 | $1,027 | $233 | $1,260 | $154 | $1,413 | $41 |

| 2016 | $1,442 | $261 | $538 | $840 | $162 | $1,002 | $238 | $1,240 | $159 | $1,399 | $44 |

| Source: IRS, Statistics of Income, Individual Income Rates and Tax Shares (2018). | |||||||||||

| Year | Total | Top 0.1% | Top 1% | Top 5% | Between 5% & 10% | Top 10% | Between 10% & 25% | Top 25% | Between 25% & 50% | Top 50% | Bottom 50% |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1980 | 100% | 8.46% | 21.01% | 11.12% | 32.13% | 24.57% | 56.70% | 25.62% | 82.32% | 17.68% | |

| 1981 | 100% | 8.30% | 20.78% | 11.20% | 31.98% | 24.69% | 56.67% | 25.59% | 82.25% | 17.75% | |

| 1982 | 100% | 8.91% | 21.23% | 11.03% | 32.26% | 24.53% | 56.79% | 25.50% | 82.29% | 17.71% | |

| 1983 | 100% | 9.29% | 21.74% | 11.04% | 32.78% | 24.44% | 57.22% | 25.30% | 82.52% | 17.48% | |

| 1984 | 100% | 9.66% | 22.19% | 11.06% | 33.25% | 24.31% | 57.56% | 25.00% | 82.56% | 17.44% | |

| 1985 | 100% | 10.03% | 22.67% | 11.10% | 33.77% | 24.21% | 57.97% | 24.77% | 82.74% | 17.26% | |

| 1986 | 100% | 11.30% | 24.11% | 11.02% | 35.12% | 23.92% | 59.04% | 24.30% | 83.34% | 16.66% | |

| The Tax Reform Act of 1986 changed the definition of AGI, so data above and below this line is not strictly comparable. | |||||||||||

| 1987 | 100% | 12.32% | 25.67% | 11.23% | 36.90% | 23.85% | 60.75% | 23.62% | 84.37% | 15.63% | |

| 1988 | 100% | 15.16% | 28.51% | 10.94% | 39.45% | 22.99% | 62.44% | 22.63% | 85.07% | 14.93% | |

| 1989 | 100% | 14.19% | 27.84% | 11.16% | 39.00% | 23.28% | 62.28% | 22.76% | 85.04% | 14.96% | |

| 1990 | 100% | 14.00% | 27.62% | 11.15% | 38.77% | 23.36% | 62.13% | 22.84% | 84.97% | 15.03% | |

| 1991 | 100% | 12.99% | 26.83% | 11.37% | 38.20% | 23.65% | 61.85% | 23.01% | 84.87% | 15.13% | |

| 1992 | 100% | 14.23% | 28.01% | 11.21% | 39.23% | 23.25% | 62.47% | 22.61% | 85.08% | 14.92% | |

| 1993 | 100% | 13.79% | 27.76% | 11.29% | 39.05% | 23.40% | 62.45% | 22.63% | 85.08% | 14.92% | |

| 1994 | 100% | 13.80% | 27.85% | 11.34% | 39.19% | 23.45% | 62.64% | 22.48% | 85.11% | 14.89% | |

| 1995 | 100% | 14.60% | 28.81% | 11.35% | 40.16% | 23.21% | 63.37% | 22.09% | 85.46% | 14.54% | |

| 1996 | 100% | 16.04% | 30.36% | 11.23% | 41.59% | 22.73% | 64.32% | 21.60% | 85.92% | 14.08% | |

| 1997 | 100% | 17.38% | 31.79% | 11.03% | 42.83% | 22.22% | 65.05% | 21.11% | 86.16% | 13.84% | |

| 1998 | 100% | 18.47% | 32.85% | 10.92% | 43.77% | 21.87% | 65.63% | 20.69% | 86.33% | 13.67% | |

| 1999 | 100% | 19.51% | 34.04% | 10.85% | 44.89% | 21.57% | 66.46% | 20.29% | 86.75% | 13.25% | |

| 2000 | 100% | 20.81% | 35.30% | 10.71% | 46.01% | 21.15% | 67.15% | 19.86% | 87.01% | 12.99% | |

| The IRS changed methodology, so data above and below this line is not strictly comparable. | |||||||||||

| 2001 | 100% | 8.05% | 17.41% | 31.61% | 10.89% | 42.50% | 21.80% | 64.31% | 21.29% | 85.60% | 14.40% |

| 2002 | 100% | 7.04% | 16.05% | 30.29% | 11.04% | 41.33% | 22.39% | 63.71% | 21.79% | 85.50% | 14.50% |

| 2003 | 100% | 7.56% | 16.73% | 30.99% | 11.03% | 42.01% | 22.33% | 64.34% | 21.52% | 85.87% | 14.13% |

| 2004 | 100% | 9.14% | 18.99% | 33.31% | 10.77% | 44.07% | 21.60% | 65.68% | 20.83% | 86.51% | 13.49% |

| 2005 | 100% | 10.64% | 21.19% | 35.61% | 10.56% | 46.17% | 20.90% | 67.07% | 19.99% | 87.06% | 12.94% |

| 2006 | 100% | 11.23% | 22.10% | 36.62% | 10.56% | 47.17% | 20.73% | 67.91% | 19.68% | 87.58% | 12.42% |

| 2007 | 100% | 11.95% | 22.86% | 37.39% | 10.49% | 47.88% | 20.53% | 68.41% | 19.40% | 87.81% | 12.19% |

| 2008 | 100% | 10.06% | 20.19% | 34.95% | 11.03% | 45.98% | 21.71% | 67.69% | 20.39% | 88.08% | 11.92% |

| 2009 | 100% | 7.94% | 17.21% | 32.18% | 11.59% | 43.77% | 22.96% | 66.74% | 21.38% | 88.12% | 11.88% |

| 2010 | 100% | 9.24% | 18.87% | 33.78% | 11.38% | 45.17% | 22.38% | 67.55% | 20.71% | 88.26% | 11.74% |

| 2011 | 100% | 8.86% | 18.70% | 33.89% | 11.50% | 45.39% | 22.43% | 67.82% | 20.63% | 88.45% | 11.55% |

| 2012 | 100% | 11.25% | 21.86% | 36.84% | 11.03% | 47.87% | 21.39% | 69.25% | 19.64% | 88.90% | 11.10% |

| 2013 | 100% | 9.03% | 19.04% | 34.42% | 11.45% | 45.87% | 22.23% | 68.10% | 20.41% | 88.51% | 11.49% |

| 2014 | 100% | 10.16% | 20.58% | 35.96% | 11.25% | 47.21% | 21.70% | 68.91% | 19.82% | 88.73% | 11.27% |

| 2015 | 100% | 10.19% | 20.65% | 36.07% | 11.29% | 47.36% | 21.64% | 68.99% | 19.72% | 88.72% | 11.28% |

| 2016 | 100% | 9.52% | 19.72% | 35.20% | 11.37% | 46.56% | 21.86% | 68.43% | 19.98% | 88.41% | 11.59% |

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe| Source: IRS, Statistics of Income, Individual Income Rates and Tax Shares (2018). | |||||||||||

| Year | Total | Top 0.1% | Top 1% | Top 5% | Between 5% & 10% | Top 10% | Between 10% & 25% | Top 25% | Between 25% & 50% | Top 50% | Bottom 50% |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1980 | 100% | 19.05% | 36.84% | 12.44% | 49.28% | 23.74% | 73.02% | 19.93% | 92.95% | 7.05% | |

| 1981 | 100% | 17.58% | 35.06% | 12.90% | 47.96% | 24.33% | 72.29% | 20.26% | 92.55% | 7.45% | |

| 1982 | 100% | 19.03% | 36.13% | 12.45% | 48.59% | 23.91% | 72.50% | 20.15% | 92.65% | 7.35% | |

| 1983 | 100% | 20.32% | 37.26% | 12.44% | 49.71% | 23.39% | 73.10% | 19.73% | 92.83% | 7.17% | |

| 1984 | 100% | 21.12% | 37.98% | 12.58% | 50.56% | 22.92% | 73.49% | 19.16% | 92.65% | 7.35% | |

| 1985 | 100% | 21.81% | 38.78% | 12.67% | 51.46% | 22.60% | 74.06% | 18.77% | 92.83% | 7.17% | |

| 1986 | 100% | 25.75% | 42.57% | 12.12% | 54.69% | 21.33% | 76.02% | 17.52% | 93.54% | 6.46% | |

| The Tax Reform Act of 1986 changed the definition of AGI, so data above and below this line is not strictly comparable. | |||||||||||

| 1987 | 100% | 24.81% | 43.26% | 12.35% | 55.61% | 21.31% | 76.92% | 17.02% | 93.93% | 6.07% | |

| 1988 | 100% | 27.58% | 45.62% | 11.66% | 57.28% | 20.57% | 77.84% | 16.44% | 94.28% | 5.72% | |

| 1989 | 100% | 25.24% | 43.94% | 11.85% | 55.78% | 21.44% | 77.22% | 16.94% | 94.17% | 5.83% | |

| 1990 | 100% | 25.13% | 43.64% | 11.73% | 55.36% | 21.66% | 77.02% | 17.16% | 94.19% | 5.81% | |

| 1991 | 100% | 24.82% | 43.38% | 12.45% | 55.82% | 21.46% | 77.29% | 17.23% | 94.52% | 5.48% | |

| 1992 | 100% | 27.54% | 45.88% | 12.12% | 58.01% | 20.47% | 78.48% | 16.46% | 94.94% | 5.06% | |

| 1993 | 100% | 29.01% | 47.36% | 11.88% | 59.24% | 20.03% | 79.27% | 15.92% | 95.19% | 4.81% | |

| 1994 | 100% | 28.86% | 47.52% | 11.93% | 59.45% | 20.10% | 79.55% | 15.68% | 95.23% | 4.77% | |

| 1995 | 100% | 30.26% | 48.91% | 11.84% | 60.75% | 19.62% | 80.36% | 15.03% | 95.39% | 4.61% | |

| 1996 | 100% | 32.31% | 50.97% | 11.54% | 62.51% | 18.80% | 81.32% | 14.36% | 95.68% | 4.32% | |

| 1997 | 100% | 33.17% | 51.87% | 11.33% | 63.20% | 18.47% | 81.67% | 14.05% | 95.72% | 4.28% | |

| 1998 | 100% | 34.75% | 53.84% | 11.20% | 65.04% | 17.65% | 82.69% | 13.10% | 95.79% | 4.21% | |

| 1999 | 100% | 36.18% | 55.45% | 11.00% | 66.45% | 17.09% | 83.54% | 12.46% | 96.00% | 4.00% | |

| 2000 | 100% | 37.42% | 56.47% | 10.86% | 67.33% | 16.68% | 84.01% | 12.08% | 96.09% | 3.91% | |

| The IRS changed methodology, so data above and below this line is not strictly comparable. | |||||||||||

| 2001 | 100% | 15.68% | 33.22% | 52.24% | 11.44% | 63.68% | 17.88% | 81.56% | 13.54% | 95.10% | 4.90% |

| 2002 | 100% | 15.09% | 33.09% | 52.86% | 11.77% | 64.63% | 18.04% | 82.67% | 13.12% | 95.79% | 4.21% |

| 2003 | 100% | 15.37% | 33.69% | 53.54% | 11.35% | 64.89% | 17.87% | 82.76% | 13.17% | 95.93% | 4.07% |

| 2004 | 100% | 17.12% | 36.28% | 56.35% | 10.96% | 67.30% | 16.52% | 83.82% | 12.31% | 96.13% | 3.87% |

| 2005 | 100% | 18.91% | 38.78% | 58.93% | 10.52% | 69.46% | 15.61% | 85.07% | 11.35% | 96.41% | 3.59% |

| 2006 | 100% | 19.24% | 39.36% | 59.49% | 10.59% | 70.08% | 15.41% | 85.49% | 11.10% | 96.59% | 3.41% |

| 2007 | 100% | 19.84% | 39.81% | 59.90% | 10.51% | 70.41% | 15.30% | 85.71% | 10.93% | 96.64% | 3.36% |

| 2008 | 100% | 18.20% | 37.51% | 58.06% | 11.14% | 69.20% | 16.37% | 85.57% | 11.33% | 96.90% | 3.10% |

| 2009 | 100% | 16.91% | 36.34% | 58.17% | 11.72% | 69.89% | 16.85% | 86.74% | 10.80% | 97.54% | 2.46% |

| 2010 | 100% | 17.88% | 37.38% | 59.07% | 11.55% | 70.62% | 16.49% | 87.11% | 10.53% | 97.64% | 2.36% |

| 2011 | 100% | 16.14% | 35.06% | 56.49% | 11.77% | 68.26% | 17.36% | 85.62% | 11.50% | 97.11% | 2.89% |

| 2012 | 100% | 18.60% | 38.09% | 58.95% | 11.22% | 70.17% | 16.25% | 86.42% | 10.80% | 97.22% | 2.78% |

| 2013 | 100% | 18.48% | 37.80% | 58.55% | 11.25% | 69.80% | 16.47% | 86.27% | 10.94% | 97.22% | 2.78% |

| 2014 | 100% | 19.85% | 39.48% | 59.97% | 10.91% | 70.88% | 15.90% | 86.78% | 10.47% | 97.25% | 2.75% |

| 2015 | 100% | 19.50% | 39.04% | 59.58% | 11.01% | 70.59% | 16.03% | 86.62% | 10.55% | 97.17% | 2.83% |

| 2016 | 100.00% | 18.12% | 37.32% | 58.23% | 11.24% | 69.47% | 16.50% | 85.97% | 10.99% | 96.96% | 3.04% |

| Source: IRS, Statistics of Income, Individual Income Rates and Tax Shares (2018). | ||||||

| Year | Top 0.1% | Top 1% | Top 5% | Top 10% | Top 25% | Top 50% |

|---|---|---|---|---|---|---|

| 1980 | $80,580 | $43,792 | $35,070 | $23,606 | $12,936 | |

| 1981 | $85,428 | $47,845 | $38,283 | $25,655 | $14,000 | |

| 1982 | $89,388 | $49,284 | $39,676 | $27,027 | $14,539 | |

| 1983 | $93,512 | $51,553 | $41,222 | $27,827 | $15,044 | |

| 1984 | $100,889 | $55,423 | $43,956 | $29,360 | $15,998 | |

| 1985 | $108,134 | $58,883 | $46,322 | $30,928 | $16,688 | |

| 1986 | $118,818 | $62,377 | $48,656 | $32,242 | $17,302 | |

| The Tax Reform Act of 1986 changed the definition of AGI, so data above and below this line is not strictly comparable. | ||||||

| 1987 | $139,289 | $68,414 | $52,921 | $33,983 | $17,768 | |

| 1988 | $157,136 | $72,735 | $55,437 | $35,398 | $18,367 | |

| 1989 | $163,869 | $76,933 | $58,263 | $36,839 | $18,993 | |

| 1990 | $167,421 | $79,064 | $60,287 | $38,080 | $19,767 | |

| 1991 | $170,139 | $81,720 | $61,944 | $38,929 | $20,097 | |

| 1992 | $181,904 | $85,103 | $64,457 | $40,378 | $20,803 | |

| 1993 | $185,715 | $87,386 | $66,077 | $41,210 | $21,179 | |

| 1994 | $195,726 | $91,226 | $68,753 | $42,742 | $21,802 | |

| 1995 | $209,406 | $96,221 | $72,094 | $44,207 | $22,344 | |

| 1996 | $227,546 | $101,141 | $74,986 | $45,757 | $23,174 | |

| 1997 | $250,736 | $108,048 | $79,212 | $48,173 | $24,393 | |

| 1998 | $269,496 | $114,729 | $83,220 | $50,607 | $25,491 | |

| 1999 | $293,415 | $120,846 | $87,682 | $52,965 | $26,415 | |

| 2000 | $313,469 | $128,336 | $92,144 | $55,225 | $27,682 | |

| The IRS changed methodology, so data above and below this line is not strictly comparable. | ||||||

| 2001 | $1,393,718 | $306,635 | $132,082 | $96,151 | $59,026 | $31,418 |

| 2002 | $1,245,352 | $296,194 | $130,750 | $95,699 | $59,066 | $31,299 |

| 2003 | $1,317,088 | $305,939 | $133,741 | $97,470 | $59,896 | $31,447 |

| 2004 | $1,617,918 | $339,993 | $140,758 | $101,838 | $62,794 | $32,622 |

| 2005 | $1,938,175 | $379,261 | $149,216 | $106,864 | $64,821 | $33,484 |

| 2006 | $2,124,625 | $402,603 | $157,390 | $112,016 | $67,291 | $34,417 |

| 2007 | $2,251,017 | $426,439 | $164,883 | $116,396 | $69,559 | $35,541 |

| 2008 | $1,867,652 | $392,513 | $163,512 | $116,813 | $69,813 | $35,340 |

| 2009 | $1,469,393 | $351,968 | $157,342 | $114,181 | $68,216 | $34,156 |

| 2010 | $1,634,386 | $369,691 | $161,579 | $116,623 | $69,126 | $34,338 |

| 2011 | $1,717,675 | $388,905 | $167,728 | $120,136 | $70,492 | $34,823 |

| 2012 | $2,161,175 | $434,682 | $175,817 | $125,195 | $73,354 | $36,055 |

| 2013 | $1,860,848 | $428,713 | $179,760 | $127,695 | $74,955 | $36,841 |

| 2014 | $2,136,762 | $465,626 | $188,996 | $133,445 | $77,714 | $38,173 |

| 2015 | $2,220,264 | $480,930 | $195,778 | $138,031 | $79,655 | $39,275 |

| 2016 | $2,124,117 | $480,804 | $197,651 | $139,713 | $80,921 | $40,078 |

| Source: IRS, Statistics of Income, Individual Income Rates and Tax Shares (2018). | |||||||||||

| Year | Total | Top 0.1% | Top 1% | Top 5% | Between 5% & 10% | Top 10% | Between 10% & 25% | Top 25% | Between 25% & 50% | Top 50% | Bottom 50% |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1980 | 15.31% | 34.47% | 26.85% | 17.13% | 23.49% | 14.80% | 19.72% | 11.91% | 17.29% | 6.10% | |

| 1981 | 15.76% | 33.37% | 26.59% | 18.16% | 23.64% | 15.53% | 20.11% | 12.48% | 17.73% | 6.62% | |

| 1982 | 14.72% | 31.43% | 25.05% | 16.61% | 22.17% | 14.35% | 18.79% | 11.63% | 16.57% | 6.10% | |

| 1983 | 13.79% | 30.18% | 23.64% | 15.54% | 20.91% | 13.20% | 17.62% | 10.76% | 15.52% | 5.66% | |

| 1984 | 13.68% | 29.92% | 23.42% | 15.57% | 20.81% | 12.90% | 17.47% | 10.48% | 15.35% | 5.77% | |

| 1985 | 13.73% | 29.86% | 23.50% | 15.69% | 20.93% | 12.83% | 17.55% | 10.41% | 15.41% | 5.70% | |

| 1986 | 14.54% | 33.13% | 25.68% | 15.99% | 22.64% | 12.97% | 18.72% | 10.48% | 16.32% | 5.63% | |

| The Tax Reform Act of 1986 changed the definition of AGI, so data above and below this line is not strictly comparable. | |||||||||||

| 1987 | 13.12% | 26.41% | 22.10% | 14.43% | 19.77% | 11.71% | 16.61% | 9.45% | 14.60% | 5.09% | |

| 1988 | 13.21% | 24.04% | 21.14% | 14.07% | 19.18% | 11.82% | 16.47% | 9.60% | 14.64% | 5.06% | |

| 1989 | 13.12% | 23.34% | 20.71% | 13.93% | 18.77% | 12.08% | 16.27% | 9.77% | 14.53% | 5.11% | |

| 1990 | 12.95% | 23.25% | 20.46% | 13.63% | 18.50% | 12.01% | 16.06% | 9.73% | 14.36% | 5.01% | |

| 1991 | 12.75% | 24.37% | 20.62% | 13.96% | 18.63% | 11.57% | 15.93% | 9.55% | 14.20% | 4.62% | |

| 1992 | 12.94% | 25.05% | 21.19% | 13.99% | 19.13% | 11.39% | 16.25% | 9.42% | 14.44% | 4.39% | |

| 1993 | 13.32% | 28.01% | 22.71% | 14.01% | 20.20% | 11.40% | 16.90% | 9.37% | 14.90% | 4.29% | |

| 1994 | 13.50% | 28.23% | 23.04% | 14.20% | 20.48% | 11.57% | 17.15% | 9.42% | 15.11% | 4.32% | |

| 1995 | 13.86% | 28.73% | 23.53% | 14.46% | 20.97% | 11.71% | 17.58% | 9.43% | 15.47% | 4.39% | |

| 1996 | 14.34% | 28.87% | 24.07% | 14.74% | 21.55% | 11.86% | 18.12% | 9.53% | 15.96% | 4.40% | |

| 1997 | 14.48% | 27.64% | 23.62% | 14.87% | 21.36% | 12.04% | 18.18% | 9.63% | 16.09% | 4.48% | |

| 1998 | 14.42% | 27.12% | 23.63% | 14.79% | 21.42% | 11.63% | 18.16% | 9.12% | 16.00% | 4.44% | |

| 1999 | 14.85% | 27.53% | 24.18% | 15.06% | 21.98% | 11.76% | 18.66% | 9.12% | 16.43% | 4.48% | |

| 2000 | 15.26% | 27.45% | 24.42% | 15.48% | 22.34% | 12.04% | 19.09% | 9.28% | 16.86% | 4.60% | |

| The IRS changed methodology, so data above and below this line is not strictly comparable. | |||||||||||

| 2001 | 14.47% | 28.17% | 27.60% | 23.91% | 15.20% | 21.68% | 11.87% | 18.35% | 9.20% | 16.08% | 4.92% |

| 2002 | 13.28% | 28.48% | 27.37% | 23.17% | 14.15% | 20.76% | 10.70% | 17.23% | 8.00% | 14.87% | 3.86% |

| 2003 | 12.11% | 24.60% | 24.38% | 20.92% | 12.46% | 18.70% | 9.69% | 15.57% | 7.41% | 13.53% | 3.49% |

| 2004 | 12.31% | 23.06% | 23.52% | 20.83% | 12.53% | 18.80% | 9.41% | 15.71% | 7.27% | 13.68% | 3.53% |

| 2005 | 12.65% | 22.48% | 23.15% | 20.93% | 12.61% | 19.03% | 9.45% | 16.04% | 7.18% | 14.01% | 3.51% |

| 2006 | 12.80% | 21.94% | 22.80% | 20.80% | 12.84% | 19.02% | 9.52% | 16.12% | 7.22% | 14.12% | 3.51% |

| 2007 | 12.90% | 21.42% | 22.46% | 20.66% | 12.92% | 18.96% | 9.61% | 16.16% | 7.27% | 14.19% | 3.56% |

| 2008 | 12.54% | 22.67% | 23.29% | 20.83% | 12.66% | 18.87% | 9.45% | 15.85% | 6.97% | 13.79% | 3.26% |

| 2009 | 11.39% | 24.28% | 24.05% | 20.59% | 11.53% | 18.19% | 8.36% | 14.81% | 5.76% | 12.61% | 2.35% |

| 2010 | 11.81% | 22.84% | 23.39% | 20.64% | 11.98% | 18.46% | 8.70% | 15.22% | 6.01% | 13.06% | 2.37% |

| 2011 | 12.54% | 22.82% | 23.50% | 20.89% | 12.83% | 18.85% | 9.70% | 15.82% | 6.98% | 13.76% | 3.13% |

| 2012 | 13.11% | 21.67% | 22.83% | 20.97% | 13.33% | 19.21% | 9.96% | 16.35% | 7.21% | 14.33% | 3.28% |

| 2013 | 13.64% | 27.91% | 27.08% | 23.20% | 13.40% | 20.75% | 10.11% | 17.28% | 7.31% | 14.98% | 3.30% |

| 2014 | 14.16% | 27.67% | 27.16% | 23.61% | 13.73% | 21.25% | 10.37% | 17.83% | 7.48% | 15.52% | 3.45% |

| 2015 | 14.34% | 27.44% | 27.10% | 23.68% | 13.99% | 21.37% | 10.62% | 18.00% | 7.67% | 15.71% | 3.59% |

| 2016 | 14.20% | 27.05% | 26.87% | 23.49% | 14.05% | 21.19% | 10.71% | 17.84% | 7.81% | 15.57% | 3.73% |

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe[1] Internal Revenue Service, Statistics of Income, “Number of Returns, Shares of AGI and Total Income Tax, AGI Floor on Percentiles in Current and Constant Dollars, and Average Tax Rates,” Table 1, and “Number of Returns, Shares of AGI and Total Income Tax, and Average Tax Rates,” Table 2, https://www.irs.gov/statistics/soi-tax-stats-individual-income-tax-rates-and-tax-shares.

[2] This data is for tax year 2016 and does not include any impact from the Tax Cuts and Jobs Act.

[3] “Average income tax rate” is defined here as income taxes paid divided by adjusted gross income.

Share this article